MARKET COMMENTARY

As we continue to evolve using the best available data to our advantage — from now on — we will make updates, as needed, throughout the calendar month instead of only one adjustment.

Thank you for the assets you have placed with us. We deeply value your trust, and we continue to work diligently to meet your investment needs by combining cutting-edge datasets from Helios with our advisors’ knowledge about your personal needs.

To ensure your portfolio most effectively serves your goals and reflects your risk tolerance, we are always available to answer any questions you may have.

To schedule a “Quick Question” 30-minute meeting regarding your portfolio or financial plans, please contact your advisor at (574) 889-7526.

ASSET ALLOCATION UPDATES

EQUITIES

Economic indicators continue to show international stocks have more opportunities than U.S. stocks, resulting in an overweight international level of exposure. (International countries have ground to make up in the pandemic recovery, proving more opportunities for economic improvement compared to the United States.) Among international markets, Italy and France have the highest economic scores.

Growth stocks continued to be preferred over value stocks — although that may change as interest rates rise. Risk-adjusted momentum is strongest in Large-Cap Growth, Large-Cap Value, and Mid-Cap Blend. Within U.S. markets, the sectors showing the highest risk-adjusted momentum continue to be Technology and Consumer Discretionary.

We made a reduction to equity exposure in some of our more conservative models, but remain with maximum equity exposure in all other models for every risk tolerance.

FIXED INCOME

Given general market volatility, convertible bonds trends turned negative, prompting their removal in favor of broader bond allocations. We maintain a tilt toward short-term bonds to manage interest rate risk.

Widening high-yield bond spreads indicate the markets are becoming more skeptical about creditworthiness, resulting in an overweight position in Treasuries to reduce risk. Also, we continue to hold bank loans, as it is the only diversifying asset class to have positive momentum.

MARKET UPDATE

The S&P 500 finished 2021 with a gain of nearly 27 percent for the year. The Nasdaq composite, powered by Tech stocks, climbed 21.4 percent, and the Dow Jones Industrial Average gained 18.7 percent. It was the third year in a row with double-digit stock market gains.

Corporate profits were up more than expected in 2021, fueled by spending as consumers increased purchases of big-ticket items and rotated more of their money toward in-person services. In addition, Wall Street got a boost from the Federal Reserve, which held its short-term interest rate near zero all year. That helped keep companies’ borrowing costs low and stock valuations high.

However, the focus is now on interest rate increases, jobs, and inflation. The Consumer Price Index (CPI) rose 6.8 percent from a year ago in November, with the fastest year-over-year increase since the 1980s. The surge in prices prompted the Fed to project three rate hikes in 2022 and double the speed of its tapering program, from $15 billion to $30 billion each month.

Despite the end of the Fed’s easy-money policies, economic growth looks to remain strong and U.S. stock market gains to be above average.

Also, the outlook for the Senate resolving the Build Back Better Act — containing proposed tax provisions — continues to dim. The Senate failed to vote before the holiday break on the roughly $2 trillion legislation, and it is unlikely that they will do so now during this mid-term election year.

HILLTOP ADVISORS’ PERSPECTIVE

We believe the economy is on solid footing and will grow well-above trend. We also expect earnings and stock prices to make fresh highs in 2022. But Covid challenges remain — in addition to supply chain disruptions, higher energy prices, and a tight labor market — and it means the markets won’t be without a level of uncertainty. The possibility of volatility is also amplified because 2022 is a big election year — both at home and abroad. A growing body of research shows that elections may influence the economy more than most executives may want to admit.

Still, we see another year of positive equity returns. 2021 ended with a superb report card with all 11 market sectors up. It’s indicative of an economy that still has strength. We believe the world economy will still enjoy strong momentum — especially when considering the average global growth over the past 30 years has been close to 3.5 percent.

Tech — the largest sector in the S&P 500 — will remain vital, along with consumer discretionary stocks. However, we have dialed back bond purchases with inflation hitting levels not seen since the early 1980s and the Federal Reserve anticipating three interest rate hikes this year.

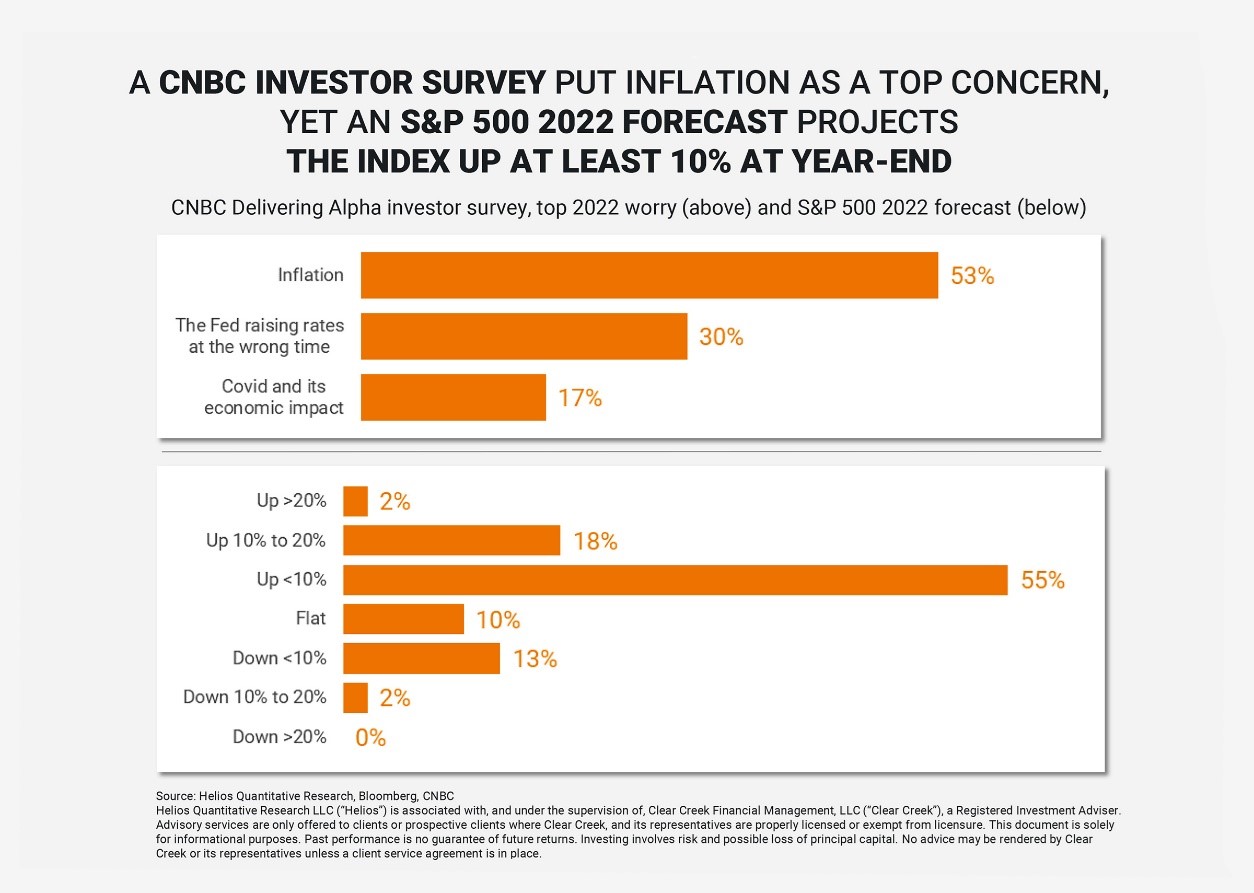

Heading into 2022, there’s growing investor unease. A recent CNBC survey shows most Wall Street investors fear inflation and lower stock market returns. Yet an S&P 500 2022 forecast projects the index up at least 10 percent at year-end.

It’s hard not to get entangled in uncertainty, and it’s why we make decisions based on quantitative analysis and not on instinct. Helios’ algorithms show the U.S. economy is set to deliver solid growth in 2022 — despite slightly ticking downward toward more normalized levels.

While the coming year will undoubtedly be defined by several critical decisions taken by the Fed, it’s important to note that asset classes — including short-term bonds, bank loans, high yield bonds, and value and growth equities — historically have fared well during prior rate-hike cycles. Of course, an inversion of the curve might cause us to reassess the signals the market is giving. But for now, the data points to the backdrop remaining positive throughout 2022.

DISCLOSURE

This newsletter is not intended to be relied upon as forecast, research, or investment advice, and is not a recommendation, offer, or solicitation to buy or sell any securities or to adopt any investment opinions expressed are as of the date noted and may change as subsequent conditions vary. The information and opinions contained in this letter are derived from proprietary and nonproprietary sources deemed by Hilltop Wealth Solutions to be reliable. The letter may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecast made will materialize. Additional information about Hilltop Wealth Solutions is available in its current disclosure documents, Form ADV, Form ADV Part 2A Brochure, and Client Relationship Summary Report which are accessible online via the SEC’s Investment Adviser Public Disclosure (IAPD) database at www.adviserinfo.sec.gov, using SEC # 801-115255. Hilltop Wealth Solutions is neither an attorney nor an accountant, and no portion of this content should be interpreted as legal, accounting, or tax advice.