The Magnificent 7 rally propelling equity markets higher was a major theme of 2023, however in December there was a glimpse of a changing story as small and mid-cap stocks significantly outperformed large cap. However, that proved temporary as the volatility in the first part of January led to mid and small cap stocks to give us most, if not all of the relatively outperformance they had versus large cap stocks. While the Magnificent 7 stocks did well in January, it was not to the degree that they did last year. The Bloomberg Magnificent 7 Index outperformed the S&P 500 by less than 50 basis points in January.

Nearly half of S&P 500 constituents have reported their sales and earnings numbers for Q4, with an aggregate sales surprise of 1.14% and earnings surprise of 6.87%. So far, Health Care has the largest sales surprise of 2.30%, where last season it also did fairly well. Utilities are reporting the most negative sales surprise again at -6.47%. Meanwhile, Energy has the largest earnings surprise at 21.55%, where it was the only sector to report a negative surprise last season. All the other sectors have reported positive earnings surprises so far, with Health Care in second at 12.07%.

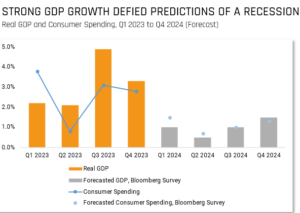

Fourth quarter GDP came in strong at an annualized rate of 3.3%, driven by a decrease in inflation that stimulated consumer spending. Consumer spending, which accounts for about two-thirds of the economy, saw broad growth across various sectors, contributing 1.9 percentage points to GDP. Personal spending rose 2.8% with gains in both goods and services. GDP is projected to grow between 0.5% and 1.5% quarter-over-quarter in 2024, according to a Bloomberg News survey.

The National Bureau of Economic Research (The NBER) evaluates key components such as Real Personal Income, Nonfarm Payrolls, Retail Sales etc… when assessing if we are in a recession or not. Payrolls came in over expectations where the outperformance was driven by gains in government and healthcare. Real personal incomes increased by 0.1%, however real personal consumption increased at a larger rate of 0.5%. The three months of gains in inflation-adjusted income are supportive of the latest retail sales report, but also point to increased use of credit to support spending habits.Looking ahead into 2024 economists are expecting consumer spending to decelerated (but stay positive) across the first half of the year and for industrial production to stay relatively tepid.

The Chinese economy is showing signs of fatigue, manufacturing has been slowing for 9 of last 10 months. Data on the Chinese economy can be both hard to come by and hard to trust, but the most recent manufacturing survey indicates the manufacturing and factory activity has been under pressure since April 2023. The weakness is despite stimulus measures the government has undertaken since the back half of last year and may mean that more stimulative measures are coming.Manufacturing weakness may compound China’s economic growth goals, already strained from the property crisis and deflationary pressures.

We remain cautiously optimistic and continue to use a quantitative investing approach. In times of uncertainty, it is more important than ever to follow the data and not make decisions based on emotions. Hilltops partnership with Helios relies on facts and data, which we use during our recalculations on a bi-weekly basis. Our models adjust appropriately to market conditions.