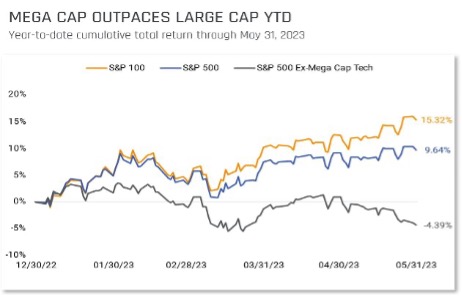

May began with a bout of volatility driven by further regional banking concerns, uncertainty related to the Fed’s continued rate policy, and headlines related to the debt ceiling. Despite early losses in the S&P 500 of just over 2.5%, the remainder of the month saw the S&P 500 recover on the back of a handful of technology companies, including NVIDIA, Meta, and Amazon. The largest US companies have contributed the majority of the gains within the S&P 500 on a year-to-date basis.

The 100 largest companies of the S&P 500 have gained over 16% YTD, while the S&P 500 is up just over 10% and the S&P 500 excluding mega cap tech, is slightly negative so far in 2023. Mega cap technology stocks have been insulated from the regional banking turmoil, and further boosted by the recent demand for AI-related items, exemplified by the major surge in the value of Nvidia in late May.

The first quarter earnings season is largely over with over 490 of the S&P 500 companies having reported results. Nearly 78% of reporting companies were able to beat analysts’ earnings estimates. While companies have been able to beat earnings estimates, overall earnings have declined 2.72% according to Bloomberg. However, companies have been able to expand their top-line revenue with over 68% percent of reporting companies growing revenue and aggregate revenue growing 4.24% across the S&P 500.

Following the Federal Reserve’s May meeting, where they increased rates another 25 basis points, the market had largely expected rate hikes to be over. Fed messaging seemed to confirm this viewpoint. However, in the latter half of May, the Fed futures market started to show a change in expectations. Towards the end of the month, the markets were placing a two-thirds probability that the Fed would further raise rates in their mid-June meeting. Instead, those probabilities came down to 26.4% by the end of the month.

At a high level, the economic data continues to suggest that a recession is not imminent and remains resilient, despite facing significant risks over the past year. While positive movements in equity markets kept equity implied volatility below its 2-year average, markets continue to try to digest mixed economic news with persistent inflation, as well as trying to anticipate what the Fed may do for the rest of the year, which can lead to sudden shifts in anticipated market risks.

We remain cautiously optimistic and continue to use a quantitative investing approach. In times of uncertainty, it is more important than ever to follow the data and not make decisions based on emotions. Hilltops partnership with Helios relies on facts and data, which we use during our recalculations on a bi-weekly basis. Our models adjust appropriately to market conditions.